18 Feb 2021

If you asked most people what they would do to keep their home if they lost their job, they would tell you anything. They would get in boarders, rent it out, get a second or third job. “You name it, I’ll do it”, we hear. Banks know this and that’s why they are happier to lend to people that are planning on living in a property. Yet more and more, we are coming across clients that are putting their home at risk before they have even bought it.

The evolving digital world has brought with it access to data, information and the ability to transact very easily. This has seen the rise of online platforms where it is easy to invest in shares and crypto currency. These all present great opportunities for people to expose themselves to investment markets and learn. However. couple that with10 years of growth in investments, with only a slight hiccup of the COVID slump, we have seen huge interest and growth in online investing.

If you were 20 in 2011, just entering your first job with surplus cash, you may have invested in shares and property and mostly seen it go up. You may have fretted a bit when COVID hit, but not for long as the markets have bounced, and bounced quickly. That’s not normal. Typically, when markets tank, they can take years to recover. If you invested in the ASX 300 index in 2008 it took 6 years to get into positive return territory. That’s after experiencing a drop of -39%.

This represents what is called a recency bias to good returns. It’s hard not to be surprised that people are getting into these investments in a big way.

Without professional advice, it also presents a huge risk to people’s financial position.

For example. I recently came across a prospective client that is looking to buy his first home. This experience inspired us to write this article. Everything looked good. When I asked where his $100k deposit was, he

advised Shares. I asked how he would feel if that dropped by 30% over night? His eyes just about popped out of his head and he asked, what do mean?

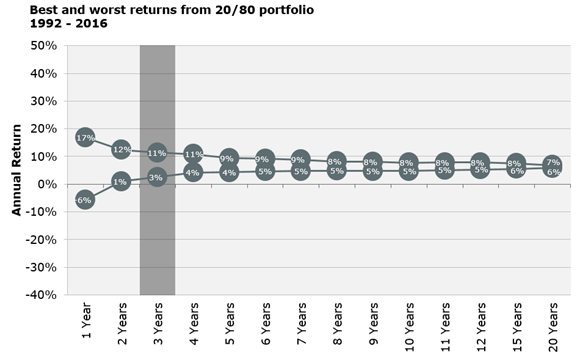

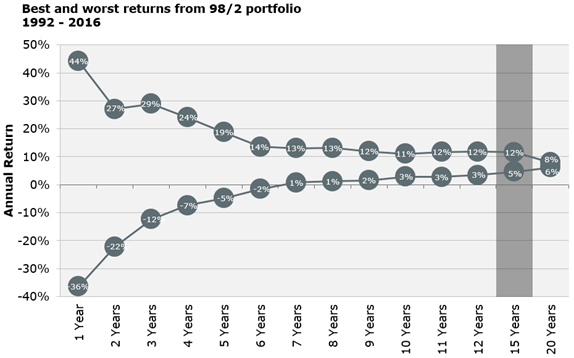

Often investments come with a recommended investment timeframe. There is good reason for this, which is illustrated below by graphs from Consilium. These graphs represent the best and worst performances of their most conservative portfolio and their most aggressive portfolios over different time frames, based on 25 years of data collection. As illustrated, the longer you are invested, the less chance you have of experiencing a loss. A conservative portfolio is made up of 80% fixed interest (defensive assets) and 20% shares and property (growth assets). The aggressive portfolio is made up of 98% growth assets and 2% defensive assets.

One of the key take outs of the graphs is that you COULD make a loss if you had to sell in the short term. If you have an offer on a property and you are relying on those funds for the deposit, that loss could come just as you are about to sell your shares.

What we are attempting to demonstrate here is the value of advice. This article relates to investment times frames and assets classes (cash/property/shares/bonds). There are many more risks you take on when you invest without advice. If you know anyone that has recently invested into shares via online platforms please share this with them. If it helps them make better investment decisions….job done!!

Disclaimer: Past returns are no guarantee of future returns. This article is meant to be engaging and informative and hopefully not a cure for insomnia. Please seek personalised advice for your situation

Property Investment is Dead. Long Live Property Investment.

Property Investment is Dead. Long Live Property Investment.

AI Boom or Bubble

AI Boom or Bubble

Mortgage Strategy VS Interest Rate

Mortgage Strategy VS Interest Rate

© 2021 AndCo Mortgages Limited. All right reserved.