14 Jun 2022

Let’s hear Independent Economist Tony Alexander’s Latest View First

In the past month forecasts for world growth have been revised downward, more evidence has emerged of troubles in the home building sector, we learnt retail spending was weaker than thought in the March quarter, and the Reserve Bank has lifted its cash rate by another 0.5%.

More than that, the Reserve Bank have brought forward the timing for interest rates peaking from mid-2024 to mid-2023 and added 0.5% to their predicted peak. Like other central banks they have decided an extra fast scramble is needed to unwind the excesses created by extremely loose monetary conditions during the pandemic.

There is good news in this. It means the interest rate pain will be over more quickly than previously thought with mortgage rates probably edging slightly lower come the end of 2023. But I retain the view expressed here a month ago that fixed rates have 0.5% – 1.0% more in rises to come.

Of high importance is the deepening woe in the household sector which I can identify from my monthly Spending Plans Survey. This is pleasing because it tells us that the spending crunch the Reserve Bank wants to achieve by raising interest rates is firmly underway. Their efforts are being helped by people putting money aside for overseas travel, concerns about the implications for economic growth of the growing brain drain, and the soaring cost of living.

People are effectively being taxed on their weekly grocery shopping and that is leaving less money free for spending elsewhere – including housing. The negatives are dominating in the real estate market and probably will continue to do so for the rest of this year. Prices are likely to keep falling into the first half of 2023 and what happens after that will depend a lot on further changes in construction costs, how big the brain drain really becomes, and the extent to which house construction rapidly falls away as buyers step back from ordering new dwellings.

For home buyers the obvious incentive is to stand back from the market for the moment. But for those with finances in order, the increasing willingness of vendors to negotiate and the 80% rise in listings from a year ago mean that it is actually becoming a better and better environment for buyers planning to hold their properties for longer than two years – which is some 96% of us.

For additional information on the economy, housing market, and interest rates, you can subscribe to Tony’s free weekly Tony’s View publication at www.tonyalexander.nz

And now from us

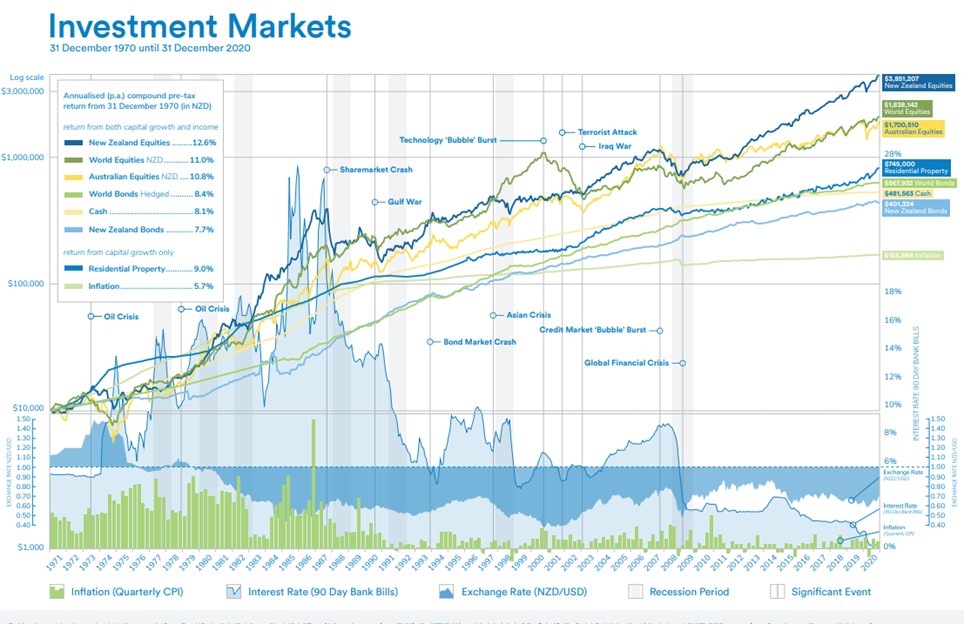

Tony’s words above reinforce a long held view that time in the market leads to better outcomes overtime, than trying to time the market. With asset prices being impacted as a result of inflation and various global events, it is natural for buyers to resist purchasing. Some homeowners look to sell to avoid further reductions in value. Here’s the catch. If you plan to be a homeowner long-term, if house prices drift lower in the short term will that have an impact on you? Only if you have to sell. When you sell, you crystalise a loss. If you plan on owning a property or developing a retirement plan over the long term, then you are likely to see short term losses regularly. However, over the longer term, you are likely to see gains as illustrated by the chart below.

What about if you sell and buy back when the market has settled. Ask yourself, when is the market settled? When prices are up? Not only have you lost money from when you purchased, but you have paid more than when you sold it. This is the same concept when you move from a growth investment fund to a conservative fund.

If you are a first home buyer, you may be hesitant to get into the market now as prices have been trending down. However, it’s important to understand what your purpose for buying is? Generally speaking, it is to have a secure place to call home for you and your family. Somewhere the landlord can’t boot you out of. If that is your purpose, then the best time to buy doesn’t matter. An exception to this is when there is less competition from other buyers and investors. Which is now. The markets could change next week. Property investors may decide that yields are now attractive given prices have hit a certain point. As soon as that happens, you’re competing against them and who will win? Highly likely to be property investors with more equity and cashflow.

Now some good news for first home buyers! Kainga Ora has run a home loan scheme for a number of years. The scheme allows first home buyers to purchase properties with as little as 5% deposit. The banks partnered with the Kainga Ora Scheme are SBS bank, Co-operative Bank, Westpac and Kiwibank. Kainga Ora underwrites the lending for the bank, taking away that low deposit risk for them.

It has just been announced that price caps have been removed for First Home Loans. The income caps remain, with an exception for single parents, for whom the cap has been lifted to $150K. The property caps still remain for access to the Housing grants.

As a result, we are seeing more applicants able to buy their first home which is fantastic news. If you live in Auckland or Wellington and are prepared to start in an apartment, that too becomes an option. If you or someone you know has been struggling to get into a home, now may be the time to talk to us.

Important date: June 30th to get your full $521 government contribution into your Kiwisaver.

Each year the New Zealand government contributes 50 cents for every dollar you contribute to you Kiwisaver account, up to a maximum of $521.43. To get the maximum contribution you need to have contributed at least $1042.86 into your KiwiSaver account before 30 June and meet certain eligibility criteria. If you need to top up your contributions, contact your adviser.

Disclaimer: This newsletter is meant to be informative and engaging, hopefully not a cure for insomnia. Please don’t take this as personalised financial advice. Discuss your situation with an Advisor. This is where I need to say past returns are no guarantee of future returns.

Property Investment is Dead. Long Live Property Investment.

Property Investment is Dead. Long Live Property Investment.

AI Boom or Bubble

AI Boom or Bubble

Mortgage Strategy VS Interest Rate

Mortgage Strategy VS Interest Rate

© 2021 AndCo Mortgages Limited. All right reserved.