22 Aug 2022

Firstly, a bear market is one that is falling. Imagine a bear tearing the market down. A market that is moving up is often referred to a bull market. Imagine a bull bucking the market up.

“Regular savings makes you love and long for bear markets” Nick Murray. Nick Murray has been a financial services professional for more than 50 years. He is among the industry’s most respected writers and speakers. What made Nick Murray make such a statement when most people detest bear markets?

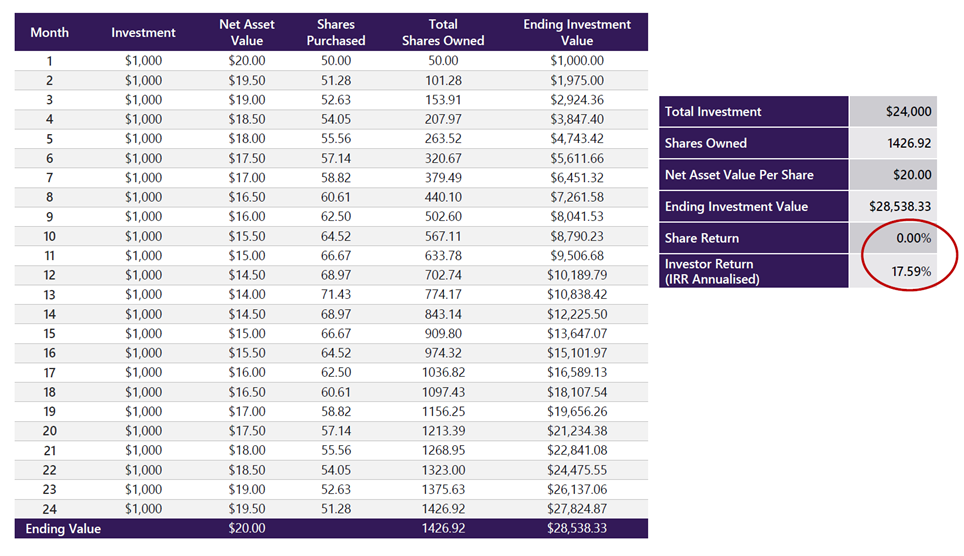

Let’s take a hypothetical scenario. Over 24 months the market returns zero. However, in the first 12 months the market drops 30%. In the next 12 months it recovers to even. An investor puts $1000 a month into their investment plan.

As you can see from month one in the table above, the shares originally cost $20 and for $1000 the investor was able to buy 50. They owned 50 shares worth $1000.

In month two, the share drops to $19.50. The investor is able to purchase 51.28, the shares owned are 101.28 and they have an ending investment value of $1,975.

In month 13 the share price has dropped to $14 and the investor is able to buy 71.43 share with their $1000 dollars. The investment has an ending value of $10,838.42.

In month 25 the share price is back up to $20 per share. Over the course of the 24 months the investor has purchased 1426.92 with an ending value of $28,538.33. The share price has not gained in that time. However, the investor has made a 17.59% return.

From independent Economist Tony Alexander

Optimism about borrowing costs

The Reserve Bank’s latest review of monetary policy has resulted in the cash rate rising 0.5% to 3.0% with a projected peak late this year or early in 2023 of 4.0%. The change has caused banks to raise their floating mortgage rates, but because fixed rate funding costs for banks reflect expectations for where the Reserve Bank’s cash rate goes in the future and not where it is now, no fixed rate rises have occurred.

The prevalent view around the world is that after aggressively raising their cash rates this year into early 2023 many central banks, including maybe our own, will need to cut them before the end of 2023 because of weak economic activity – potentially a global recession – and rapidly falling inflation rates.

The theory is a good one but vulnerable to wishful thinking. None of us predicted the recent surge in inflation so we have to be careful not to treat too seriously the new view of inflation easing rapidly. None of us knows what will happen with China’s Covid eradication policy and whether it will continue to disrupt supply chains and keep prices from easing.

We certainly don’t know what will happen with food and energy prices as a result of developments in Russia’s war against Ukraine. And how exactly wages growth responds to tight labour markets is still largely guesswork at this stage.

What this means is that although fixing for just one year or floating one’s mortgage rate would seem optimal if one purely bases the decision on forecasts of where inflation and interest rates are headed, caution would suggest perhaps some diversification. That is, borrowers should not completely rule out having a portion of their debt fixed for a two or even three year period – just in case the economic models fail again – as they unfortunately have done since 2007.

For additional information on the economy, housing market, and interest rates, you can subscribe to Tony’s free weekly Tony’s View publication at www.tonyalexander.nz

Disclaimer: This newsletter is meant to be informative and engaging, hopefully not a cure for insomnia. Please don’t take this as personalised financial advice. Discuss your situation with an Advisor. This is where I need to say past returns are no guarantee of future returns.

Property Investment is Dead. Long Live Property Investment.

Property Investment is Dead. Long Live Property Investment.

AI Boom or Bubble

AI Boom or Bubble

Mortgage Strategy VS Interest Rate

Mortgage Strategy VS Interest Rate

© 2021 AndCo Mortgages Limited. All right reserved.